Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

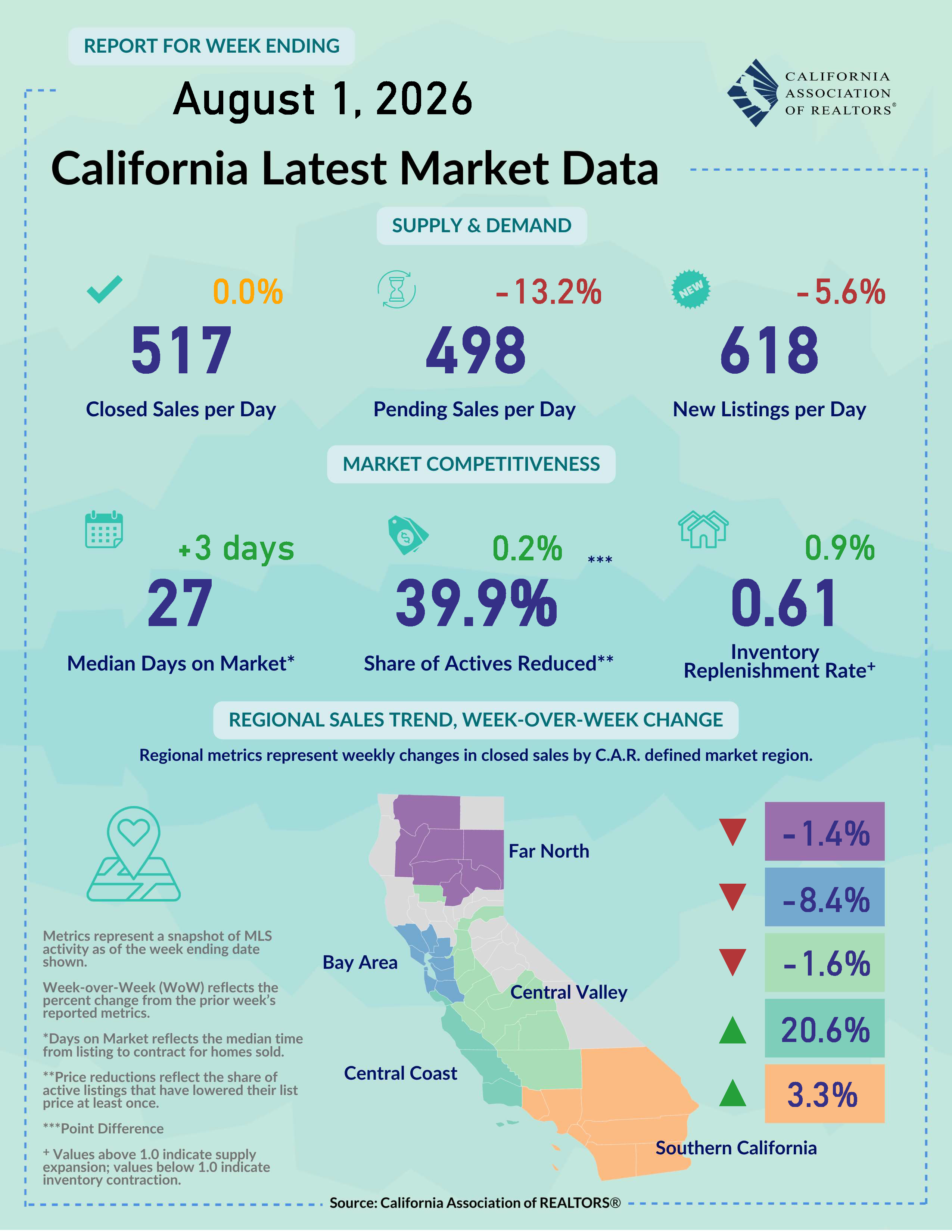

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

The RAA: Protecting REALTORS® and Homeownership REALTOR® Action FundC.A.R. Senior Vice President Sanjay Wagle sits down with former Senate Majority Leader Emeritus Robert Hertzberg to discuss the proposed Middle-Class Homeownership and Family Home Construction Act.

Learn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

August 3, 2026 - The U.S. economy lost a little steam in the second quarter of 2026 as real GDP growth cooled to 1.5%, but consumer spending accelerated due partly to bigger-than-usual tax refunds. The Federal Reserve left its benchmark federal funds rate unchanged for a fifth consecutive meeting, but three regional bank presidents dissented in favor of a rate hike, signaling lively debate over how to address stubborn inflation. Consumer confidence slipped again in July as households were less positive about current business and labor market conditions. Construction declined in June with homebuying numbers softening with elevated mortgage rates. Together, these developments point to an economy that continues to expand, but with momentum becoming more uneven as consumers, businesses, and the housing market adjust to persistent inflation and higher borrowing costs. Real GDP growth came in at 1.5% in the second quarter of 2026: Real gross domestic product (GDP) grew at a 1.5% annual rate in Q22026, according to estimates from the Bureau of Economic Analysis released on July 30, down from 2.1% in the first quarter and short of the 2.1% forecasted by polled economists. Consumer spending, investment, and exports led to GDP growth, which was partially offset by a decrease in government spending and an increase in imports. Underlying private demand was strong: real final sales to private domestic purchasers - the sum of consumer spending and gross private fixed investment - increased by 3.9% in the second quarter, up from the first. Price measures moved higher, while the gross domestic price index rose 5.7%. Within investment, gains in equipment and intellectual property products increased, offset somewhat by a drop in manufacturing. With the Middle East conflict remaining unsettled and energy prices staying elevated, the economy will likely have a more modest growth in the next six months but continue to stay positive. Fed holds rates steady as three officials dissent: The Federal Open Market Committee (FOMC) voted 9-3 to keep the federal funds rate target in a range of 3.5% to 3.75%, the same rate it has been throughout 2026. The three dissenting voices were the first time since 2016 that three policymakers dissented in the same direction; in this case, each preferred a rate hike to combat inflation. The post-meeting statement, the first from new Chair Kevin Warsh, described expanding economic activity despite uncertainty tied to the conflict in Iran. Warsh characterized productivity growth and capital investment as strong. Job gains have largely kept pace with the workforce and the unemployment rate remains low. The FOMC said inflation remains elevated relative to its 2% goal, in part due to energy shocks. Predictions from the committee put the year-end rate between 3.6% and 4.1%. The next FOMC meeting will be held in September. Consumer confidence edges lower: The Consumer Board’s Consumer Confidence Index fell by 1.4 points to 90.8 in July, down from an upwardly revised 92.2 in June and below the 92.4 expected by forecasters. The Present Situation Index explains the decline, which dropped 3.6 points in its third consecutive monthly decline. The Expectations Index remained unchanged but remains below the 80 threshold that historically signals a recession. It has been below 80 since February 2025. Net views of current business conditions declined by 2.6 percentage points. The labor market differential - the share of respondents saying jobs are plentiful minus the share saying they are hard to get - slipped 3.1% as fewer respondents described jobs as plentiful. The Conference Board’s Chief Economist Dana Peterson noted that consumers anticipate little improvement in business conditions in the next 6 months. Inflation expectations eased somewhat and views of current family finances improved, but write-in responses continued to focus on food and grocery prices increasing. With oil prices spiking up sharply in recent weeks, inflation will likely see more upward pressure and may not come back down to the pre-war levels soon if the war lingers on. Construction spending slipped in June as homebuilding weakened: The Census Bureau reported this morning that construction spending in June ran at a seasonally adjusted annual rate of $2,166.5 billion, 0.1% below the revised May estimate of $2,168.5 billion and well short of the 0.2% gain anticipated by economists polled by Reuters. The latest figure is 3.2% below the June 2025 estimate of $2,237.7 billion, and spending across the first six months totaled $1,046.9 billion, 3.5% below the comparable 2025 period. Private construction eased 0.1% after a 0.2% decline the prior month. Residential investment dropped 0.3%, with outlays on new single-family projects off 0.6% for the month and 3.3% from a year earlier, while multifamily spending fell 0.7%. Private nonresidential spending inched up 0.1% to $745.3 billion, though factory projects fell 1.2%. Public construction was essentially flat at $544.1 billion, with both state and local and federal outlays unchanged. Highway construction came in at $150.9 billion and educational construction at $113.1 billion. Higher borrowing costs remain the culprit: Freddie Mac put the 30-year fixed mortgage at a one-year high of 6.66% last week, nearly 70 basis points above where it stood at the end of February. With geopolitical uncertainty likely lingering on in the next few weeks, building activity could remain soft in the coming months. Rental market conditions tightened up in July: Housing demand in the apartment rental market continued to improve gradually as the end of the summer season approaches but overall conditions remain relatively cool, according to the latest Apartment List Rent Report. The national median rent in July increased 0.2% month-over-month to $1,388, inching up for the sixth consecutive month. On a year-over-year basis, median rent remained below last year’s level with a decline of 1.1%, the smallest dip in the last seven months. Meanwhile, the average national vacancy rate for multifamily homes staying put at 7.2%, with the list-to-lease time virtually unchanged at 30 days. At the metro level, three areas in California were on the top 10 fastest year-over-year rent growth list in the U.S., with San Francisco (9.4%) and San Jose (7.6%) taking the top two spots, while Fresno (2.2%) came in at number 8. With uncertain macroeconomic outlook continues to present risks to the rental demand, the rental market may see a plateau if the war continues in coming months. Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

|